The Kaplan & Norton Balanced Scorecard is a key feature within Corporater BMP (Business Management Platform) that offers end users an effective means by which a powerful business strategy can be developed and monitored. It was formulated by Robert Kaplan, Professor of Leadership Development at Harvard Business School, and business theorist David Norton. The Balanced Scorecard model was first presented in a 1992 edition of the Harvard Business Review, and was subsequently adopted by thousands of private, public and non-profit organizations, becoming a standard practice in the articulation of business strategy.

In a republishing of the article from 2007, the Harvard Business Review acknowledged that the Kaplan & Norton Balanced Scorecard “revolutionized conventional thinking about performance metrics.” It was also stated that the Balanced Scorecard “has given a generation of managers a better understanding of how their companies are really doing.”

THEORY OF THE BALANCED SCORECARD

The Balanced Scorecard is predicated upon the mission, vision and values that an organization aims to realize or embody.

The mission is a brief statement that expresses the basic purpose of the organization. It will inform both executives and their employees of the cause for which the have come together, and the products or services they are to provide.

The vision is more specific in that it states the goals an organization seeks to achieve within 3-10 years. Whilst the mission focuses more internally, the vision is more market-oriented and aspirational in tone, seeking to communicate how the organization wishes to be viewed. The vision should also be specific and quantifiable, stating the specific success measurement in terms of profitability, the specific niche of the organization (e.g. leading EPM solution provider), and the time frame in which this is to be achieved.

A values statement presents the behavior, character and culture of an organization, seeking to explain why these are important. These will include providing quality products or services, investing in employees and corporate social responsibility.

The methods by which to achieve these fundamental objectives are detailed by four key perspectives from which to view business strategy: financial, learning and growth, customers, and internal processes.

1. Financial

The Financial Perspective is the most familiar within the Balanced Scorecard, being concerned with traditional financial performance measures such as net income and return on investment, providing an overall assessment of organizational profitability.

In contrast to more traditional management structures which emphasize long-term financial goals, the Balanced Scorecard features three additional perspectives which measure the progress of an organization in strengthening its intangible assets. In tracking the development of these assets, the ability of an organization to achieve its long-term financial objectives is enhanced due to a more comprehensive business strategy.

2. Learning and Growth

This perspective accounts for the ability of an organization to change and improve. It is largely focused on the corporate culture of an organization and considers how it can maximize the efficiency of employees by teaching new skills and imparting key information. This could include training and certifications in addition to knowledge of relevant market trends.

3. Customers

The Customer Perspective focuses on customer satisfaction and business development. It examines how an organization is viewed in comparison to its competitors and questions how a competitive advantage can be gained within a market. The overall marketability of relevant products and services are also monitored and may involve surveys in order to gauge outcomes.

4. Internal Processes

This perspective considers the overall efficiency of an organization and charts the processes necessary to achieve objectives whilst considering performance and continuous improvement. Processes are monitored for their ability to increase customer retention whilst also satisfying shareholder expectations. Performance data is then gathered in order to analyze process impact.

Image 1: The Four Perspectives

Each Perspective consists of strategic objectives which state how a strategy relating to a specific area of business activity will be made operational. Examples in this regard may include revenue targets, cost-effective products and services for customers, certification opportunities for employees or improving the efficiency of resource utilization.

Each strategic objective contains a set of KPIs (Key Performance Indicators), which state how effectively an organization performs a given function, and whether strategic objectives are being met. From this, it is possible to determine whether an organization and its business strategy is effective by clearly displaying possible disparities between actual and targeted outcomes.

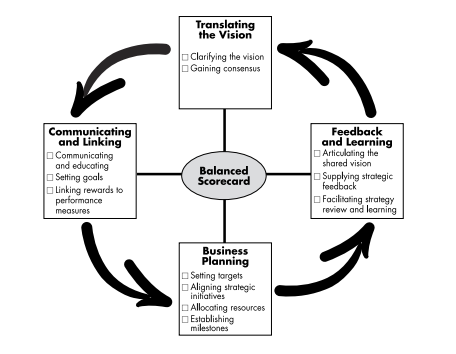

The Balanced Scorecard integrates these four perspectives with four management processes that work both separately and in combination, to break down long term objectives into smaller, actionable goals.

1. Translating the Vision

This process emphasizes the specification of goals, rather than relying on vague, general aims and objectives. Specific strategic objectives are drawn from the four perspectives in order to set out a concrete business strategy, which constitutes the result of reconciling differing interpretations among executives regarding the basic organizational vision.

2. Communicating and Linking

Kaplan and Norton emphasized the need to disseminate the Balanced Scorecard throughout the organizational structure. Whilst a high-level, overall organizational scorecard can exist, each individual unit within the structure is enabled to possess its own, which converts business strategy into specific unitary objectives and measures. This also allows for a granular approach, where personal scorecards can exist for each employee, allowing them to understand their individual impact on the implementation of the overall business strategy.

3. Business Planning

The Balanced Scorecard integrates strategic planning with budgeting, where typically these two activities are treated separately under other strategy models. When performance measures have been agreed within the company, the most important drivers of performance are identified and monitored in order to consolidate progress.

4. Feedback and Learning

By including a feedback component, the Balanced Scorecard allows for the adjustment of approaches with reference to available metrics. This can include feedback concerning any area of business operation which can be integrated into the scorecard, allowing for the refinement of business strategy.

Image 2: Management Processes

When applied to a specific strategic objective, these management processes can be used to discern specific strategic initiatives that can allow an organization to successfully implement its strategy

CONCLUSION

The Balanced Scorecard is a dynamic concept for business strategy. In the next article, we will present the Balanced Scorecard as a function within Corporater BMP, in order to further demonstrate the value of this solution. Clariba also recognizes the value of the Balanced Scorecard, possessing consultants who appreciate its utility, and having used the model to articulate our own 2020 Plan. With this model acting as the fundamental structure of our own business strategy, we are confident in our ability to realize our own strategic mission and vision in the near future.

REFERENCES

https://corporater.com/en/balanced-scorecard-solution/

https://hbr.org/2007/07/using-the-balanced-scorecard-as-a-strategic-management-system

Image 1 - Screenshot, Corporater BMP Power User Course

Image 2 - https://hbr.org/2007/07/using-the-balanced-scorecard-as-a-strategic-management-system